As we still digest this week’s U.S. Non-Farm Payrolls report, I have put together an overview of what is going on in the world, and where I think we are heading.

In particular I have recently been thinking a lot about inflation, or lack of any, that we are witnessing on a global scale. Whether this trend reverses in the coming months will be extremely important for both Wall Street and Main Street.

I am pretty confident that this will not happen, that deflation or flat lining prices are here to stay, and this will lead to anaemic growth for quite a few years, as debt sustainability will continue to be an issue. Here’s why.

The main reference for the discussion that follows is the latest Geneva Report on the World Economy, as its analysis and its conclusions are very much in line with mine. It is an extremely well presented and well researched paper, with a ton of information (and a lot of useful charts, some of which I borrowed) and I strongly recommend it as a read. You can find a summary by the authors on Voxeu.org and the full paper here.

Lever up before you go go

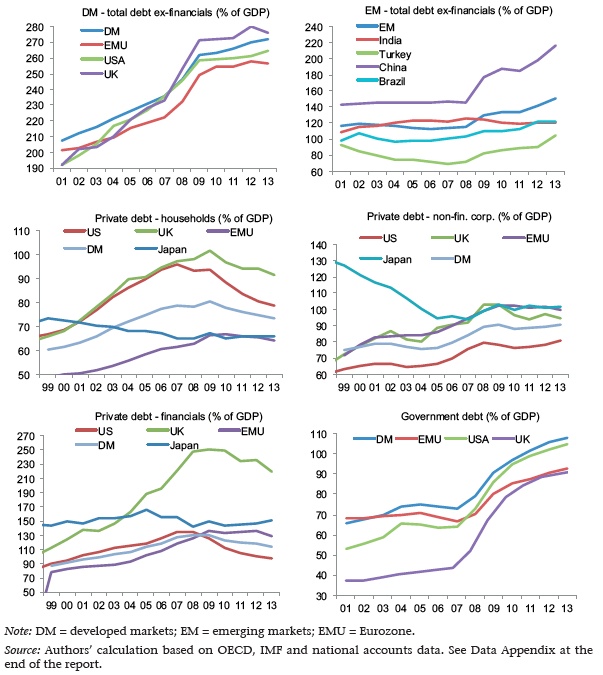

One of the culprits of the 2008 financial crisis was, as has been widely discussed by several observers, the excessive amount of debt that both individual and financial institutions had taken on, based on too-optimistic assumptions about future growth and earnings. Since the crisis hit, the following things have happened:

- the public sector has taken over a large share of the private sector’s debt;

- deleveraging has barely even started, with global debt levels at all time highs;

- while developed markets’ leverage and debt accumulation has stabilised, albeit at very high levels, emerging markets have increased their debt burden substantially, with China playing a major role here.

Source: 16th Geneva Report on the World Economy

As we now start tackling this huge amount of debt, global spending and growth will continue being impaired, keeping prices low globally.

This will be true both in the US, in Europe and in Asia, although for slightly different reasons in each case, and each face different challenges.

The US: a recovery, only for a selected few.

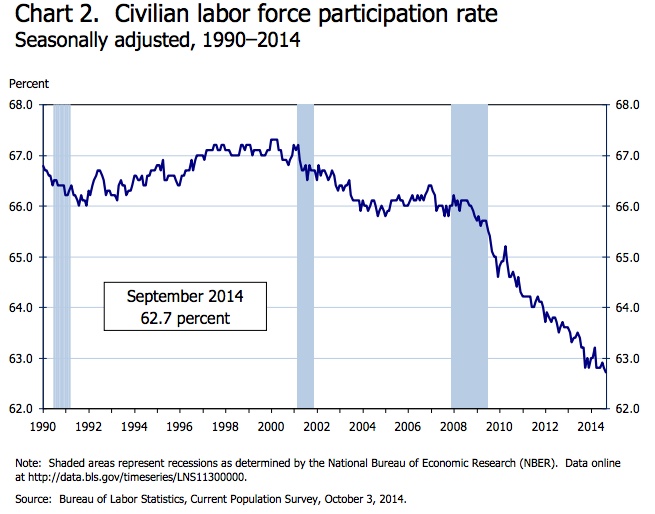

Wages are not growing, inflation is not going anywhere, and the unemployment rate has been trending lower mostly thanks to a drop in the denominator, with the participation rate in continuous decline as retiring baby boomers and low-skilled workers exit the workforce altogether. Some of the latest stats released by the BLS do give encouraging signs, with less part-time workers in the mix, but nevertheless the situation is far from encouraging. People are not making money, they have to agree lower wages to get a job, and hence are spending less.

BLS participation rate chart – October 2014

“Yes, but what about the boom we are seeing in tech?”

I love technology, I think we are now seeing a true revolution in science, technology, manufacturing (think that you will soon be able to make anything you’ll want from your sofa, with a pc and a 3D printer), but this is only going to benefit the capital owners, the entrepreneurs, and not the majority of the workforce. Although they do contribute greatly to the economy’s value added, tech companies only employ a relatively small number of people. The winners are the founders and the VCs, who, even if they start spending money like crazy, will do little to compensate the lower wages that low skilled workers now have to accept.

On a broader basis, we have seen very little investments being done by corporates (or by the government for that matter. See an earlier post on this topic here), who would rather use the cash piles to buy back shares, taking advantage of the currently low level of rates to boost leverage still, to keep ROE at the same level, despite the anaemic demand, and are essentially saying to their shareholdes “Gentlemen, here’s your money back, we really don’t know what do to with it.”

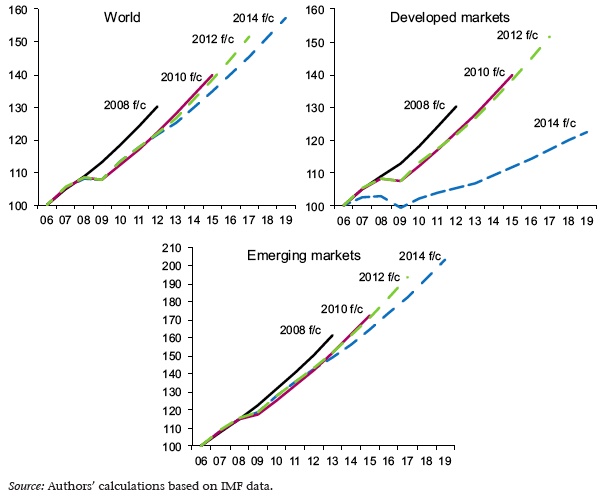

All this is propping up the stock market, but for the wrong reasons. Perhaps equity investors’ assumptions about future earnings are optimistic, but with global demand still very slow it’s a rich assumption to make, with previous growth estimate having proven optimistic several times already.

IMF GDP forecast vintages (GDP levels, 2006=100)

Source: 16th Geneva Report on the World Economy

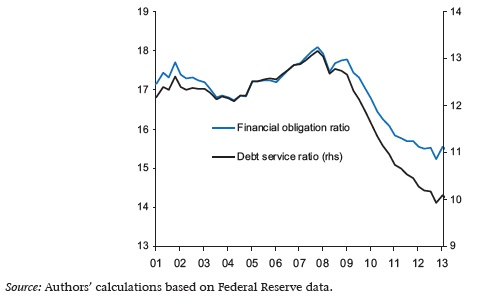

Having said this, the U.S. economy has faced the crisis sooner and better than other countries, with the private sector in a better shape than before the crisis, personal debt being reduced, and financial institutions balance sheets looking healthier after the several rounds of capital injections and writedowns.

Household debt-carrying costs (% of disposable income) Source: 16th Geneva Report on the World Economy

Europe, on the other hand, is about to face its demons.

Europe: the ship is sinking.

They say that timing is everything, but I don’t think the European policymakers got that memo.

Whereas in the US, a concerted effort between the Treasury and the Fed allowed banks to be promptly recapitalized and leverage reduced, providing the economy with a cushion to face the blow from the housing collapse, Europe’s inadequate institutional framework, as well as a lack of coordination and disagreements between member States with regards to the best course of action, meant that fiscal adjustments were not met by an adequate monetary policy easing.

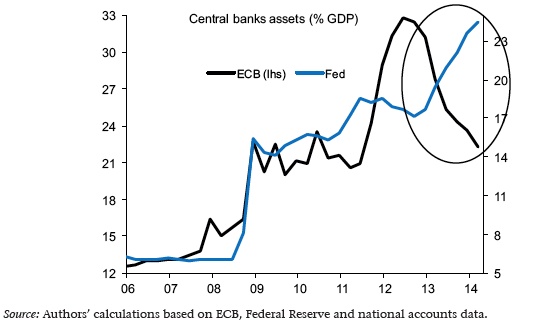

As governments tightened the belt, the ECB had, and still has, in many respects, its hands tied and could not counteract the subsequent blow to economic growth. Despite its early efforts, via several refinancing operations aimed ad keeping the banking system alive, it was too little to late, and if anything it now sees its balance sheet shrinking as those loans come due and are repaid. Mario and co. have a lot of catching up to do, and it seems pretty clear that a full scale round of asset buying is around the corner (or so the market seems to think).

Federal Reserve and ECB balance sheets

Source: 16th Geneva Report on the World Economy

Would this solve the problem? If only it was that easy… Taking a hint from the Japanese experience, if every bond bought by a central bank translated in 1bp of economic growth, Japan would probably be one of the wealthiest and fastest growing countries in the world, which it clearly isn’t. By the same token, the ECB cannot, on its own, steer the ship away from the icebergs. Structural reforms at are badly required, European countries need to work to regain competitiveness by easing labour markets and cutting red tape (I am Italian, trust me, I know what red tape looks like…). I could go on forever talking about this but this is probably a good topic for a separate note.

The bottom-line is that the probability of a concerted effort at European level is very very unlikely. European politicians’ poor track record does not make me optimistic about the economic prospects for the region, as the data continues to show. We will see action only when national politicians will feel forced into a corner. I think we are going that way, but we are not just there yet.

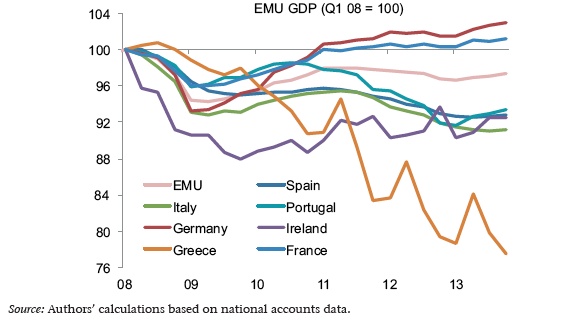

In the meanwhile, Europeans are dissaving to prevent their living standards from falling, and are, most definitely, becoming more conservative when it comes to spending, paving the way for deflation. And when you have countries with Debt/GDP ratios north of 150pc (Italy), deflation is the last thing you want.

Eurozone and selected member countries’ output levels

Source: 16th Geneva Report on the World Economy

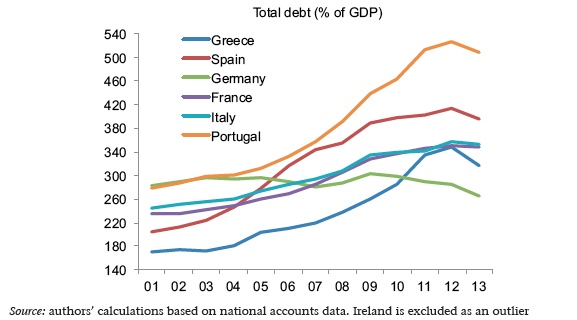

Selected Eurozone countries’ total debt

Source: 16th Geneva Report on the World Economy

Next stop: Asia?

Having learnt (you would hope) the lessons from past crises, emerging markets faced the 2008 financial crisis in better shape than most developed economies, with low external debt, a high savings ratio, and vast amounts of foreign exchange reserves. This did allow them to weather the storm and continue growing at the rapid pace that most of them had been enjoying since the late 1990s.

The disruption in global demand, however, begun more recently to impact their mostly export driven economies, and saw them reacting via a rapid expansion in domestic credit, with each country. Emerging market economies, and China in particular, are still seeking to rebalance away from external demand and more towards a domestic demand driven growth.

As discussed in the GWRE, the credit boom did help to push Chinese growth above potential for several years, but also led to inefficient investments and overcapacity in several sectors (steel, construction). This is now proving to be clearly an unsustainable path, and domestic GDP has been gradually adjusting lower for a while.

In an environment where leverage is now 220% of GDP, the Chinese government is slowly steering the economy and managing selective defaults, and will probably be able to wear the impact of the slowdown thanks to the low level of government debt, but the reduction in global demand, as 1 billion people spend money at home rather than on foreign goods, will continue to be felt and it is difficult to see how this is not going to weigh on prices globally.

China total debt and breakdown

Source: 16th Geneva Report on the World Economy

Implications for asset markets

The low level of rates that we have been enjoying is probably going to be with us for a while, given the grim outlook for inflation globally, and despite the Fed’s dual mandate and better U.S. economic performance will probably allow them to hike rates at some point in 2015, it is by no means a given than it will be the beginning of a hiking cycle as the ones we have witnessed in the past. In this I agree with Adam Posen’s view.

The last crisis has been detrimental not only for actual output, but also for potential output, marking lower the equilibrium level of yields that the Fed will have to target going forward. I doubt we will see a massive jump in yields in the 10yr. and 30yr. sector, in light of the growth and inflation dynamics that are on the horizon, unless we see a push towards more investments, increasing the economy’s potential output. Given that the U.S. is, nevertheless, further ahead in the rebalancing process than most other countries, and see its real yields rise sooner than others, we will continue to see the USD on a steady appreciation path, particularly versus EM currencies.

Most U.S. stocks are now at levels that defy gravity, with investors hunting for returns and continuously pushing farther along the risk spectrum, and some valuations that could be hard to justify if my view of future economic growth, and therefore earnings, is correct.

The central bank put, though, is still going to be at the back of investors’ mind, and therefore I find it unlikely that we will see a crash, but rather a gradual repricing lower. In this I do agree with the latest thoughts from Absolute Return Partners (via ValueWalk).

The situation in Europe does not bode well for European stocks, although companies with larger shares of exports outside the EU will benefit from the USD appreciation and overall outperform the rest. The single currency is Draghi’s best friend these days, and helping in easing financial conditions (how much European financial conditions depend on the currency is open to debate, with the majority of trade happening within the European borders). Ultimately, whether we do see a meaningful round of QE by the ECB will drive the currency and European asset markets. I think they will have to do something big, but the lower the currency moves, the bigger the scope for disappointment.

European government bonds are unlikely to selloff in the current environment, as deflationary dynamics push real yields higher and as lower prices materialise pressure will increase on the ECB to act.

EM assets, currencies, equities and fixed income, are in for a tough few months, and the negative impact of low growth numbers globally, as well the potential for a Fed hike, has already started being priced in. As discussed in an earlier post, EM countries have enjoyed a great run over the last few years, and have taken advantage of low yields by attracting foreign capital, and issuing debt, with corporates particularly exposed to external liabilities and currency mismatches. At sovereign level, risk premium is likely to rise and stay for the countries that have seen worsening current account deficit, have low foreign exchange reserves and are particularly reliant on commodities exports in a world where commodity prices are likely to remain low or fall further. EM countries that benefit from higher domestic savings, lower leverage, and healthier current account balances are probably a better play. India in particular is going to benefit from further inflows as Rajan and Modi’s work to make the political and financial environment friendlier for investors (see a previous focus post on India here).

Stretched positioning will have to reckoned with on a regular basis, but at the same time will allow late entrants to find decent entry levels.

Chinese assets could suffer if the government misjudges how much the economy is slowing and how much the increase in leverage we have seen to date will impact domestic demand. The currency is probably going to be the first escape valve in this case.

Last but not least, commodities and commodity currencies are likely to continue on their downward trajectory, in a world with falling prices and anaemic growth and trade dynamics.

Do we really Need inflation for having higher yield in the 10 – 30 years gov bonds? How about discounting the massive credit risk generated by the fact there’s no apparent limit to the debt/gdp ratio for most of the countries around the world.

One comment on the central bankks giudelines : the more you insist on giving interest rate and time giudence the less you get in terms of rates. Entrepreneurs will simply react ( rationally) by waiting till the last minute before asking for some money and investing it ; they have no visibility and there’s aggregate demand out there how can we pretend they junp on the bandwagon of free investing and spending? The longer they wait the more growth will slow down

LikeLiked by 1 person

Hello Roberto. Here’s what I think.

Re credit risk premium, I would argue that’s more relevant for countries where current account dynamics have been going in the wrong direction, with a widening deficit, or a shrinking surplus, especially if met with a deteriorating government budget balance.

I don’t think this applies to the US, but rather more to countries such as the UK and Japan, where risk premium is going to continue rising, I think. The UK in particular, is experiencing a twin deficit, as discussed by David Smith’s in his Sunday Times column (http://www.economicsuk.com/blog/002051.html) with falling wages and and increased reliance on foreign capital to finance its debt. Both currency and yields should adjust to make it worth it for foreigners to pile into UK assets at higher and higher prices.

The Japanese case, i don’t have to tell you, has been going on forever, with people puzzled by how longer they can sustain their debt levels for so long. The fact that domestic savers have been holding most of the JGBs has been used as a reason, but as that’s changing, premium is going to have to rise to lure them into keeping the money at home rather than abroad. This could get people asking whether, as money starts flowing out of the country, and with Japan now with a C/A deficit, debt sustainability is an issue. I think yields will rise accordingly, but as of now, the currency will continue to be the first to adjust.

I could add other examples, among the commodity producing countries in particular (Australia, NZ, South Africa), but the story is basically the same.

Lastly, to comment on the US case, despite the amount of the debt that they still have to deal with, I think they have done quite a bit of work post crisis to leverage the system, and with their trade balance now looking healthier as they are now becoming the world’s largest oil producers, they now look as the best of a bad bunch from the point of view of credit risk and debt sustainability. That, combined with a lower level of structural growth should help contain any meaningful increase in long term yields.

If you have any more thoughts, I’d be happy to read them!

LikeLike

One more thing, re inflation and the tech boom we are seeing…. just to reinforce the argument…

“Volkswagen to replace retiring baby boomers with robots”

http://www.ft.com/cms/s/0/4337b9a0-4d6b-11e4-bf60-00144feab7de.html#axzz3FH18JB3f

Not sure how this can be inflationary.

LikeLike