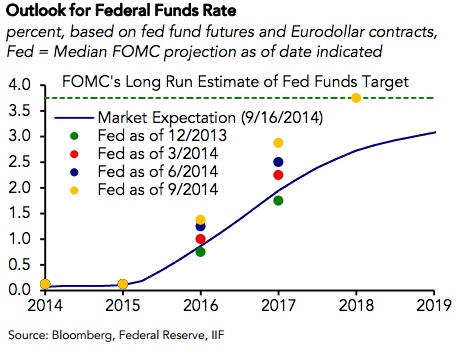

This week’s FOMC meeting got quite a few observers worried that the market might be pricing in too benign a path for US rates when compared to the median forecasts for Fed Funds issued by the Committee for the next two years.

As markets start getting a little jittery, three themes in particular have caught my attention, amidst the ton of material that has been published over the last few days. Here’s an overview, with links to all relevant references. And no, I won’t mention Scotland…

Deleveraging? What deleveraging?

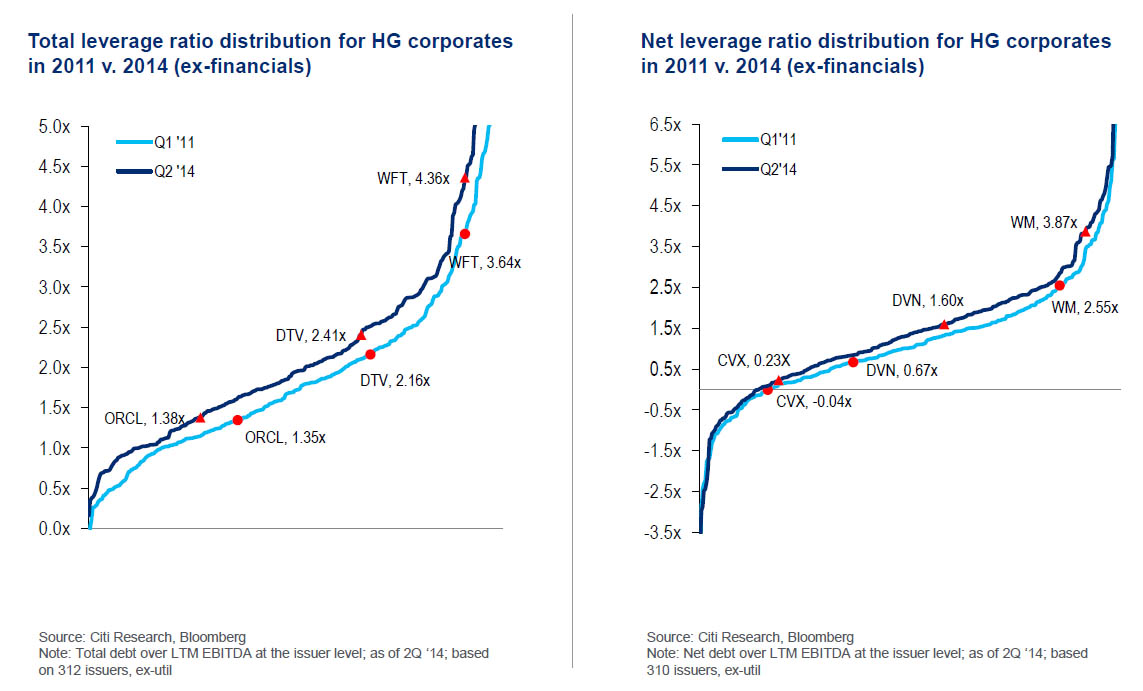

Despite all the talk about deleveraging taking place since 2008, and about US households cleaning up their balance sheets (US private sector debt was revised lower by 13pc of GDP last week), we are still far away from the safe zone, and whatever credit individuals choose to avoid has been taken up, in size, by the corporate sector.

When Citi analyst tried to answer the question “Who’s levering up?”, they finds that leverage has actually never been higher

“Pretty much everybody. We calculate leverage for the IG universe today and three years ago (leverage ratio on the Y axis, names on the X axis and ordered from most to least levered). In gross and net terms there has basically been a parallel shift upward.”

The same can be seen when looking at the effect of share buybacks, aimed at increasing balance sheet leverage via an increase in assets vs. equity.

EM. This time is different. Or is it?

Emerging markets have benefited from investor flows, with no replay of the selloff driven by the beginning of the Fed tapering in 2013, at least so far.

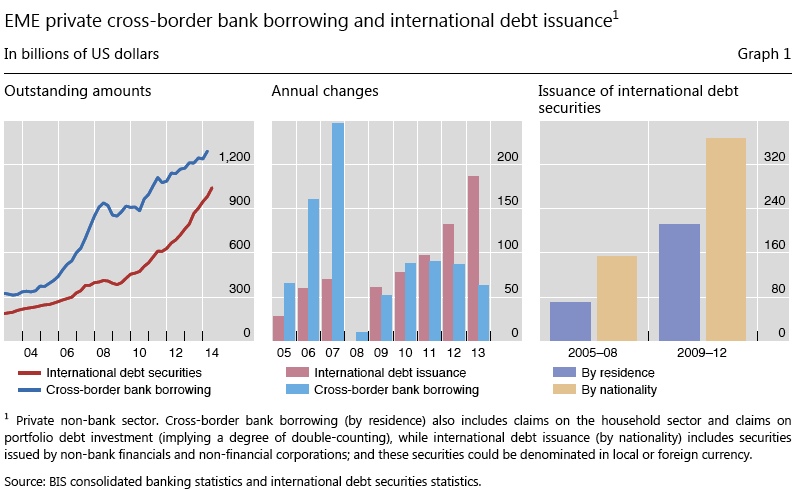

The BIS has written extensively about EM in their latest Quarterly Review, and looked at two areas in particular that could be a source of concern

- Over the last 10 years, the share of global AUM invested in EM has increased considerably, and asset managers now hold a large share of EM fixed income and equity markets, while venturing farther and farther afield in search for the yield that they could not find in developed markets.

As the Fed and the BoE prepare to hike rates, and expected returns in G10 start to rise again, some of the money currently in EM could see its way back home, only to find that the exit is too small for everyone to get out quietly.

- EM corporates have exploited the easy financial conditions globally by increasing balance sheet leverage, and ramping foreign currency borrowing. Although one could argue that capital raising could have a positive effect on a company’s value if used as a vehicle to finance investments which would then increase future profitability, data shows that most of the funds raised by EM corporates has been parked into deposits, earning the carry. This raises concerns about rollover risks and currency mismatch in an environment where the USD is poised to continue appreciating.

Emerging market assets have been relatively resilient, despite the increased volatility driven by local political shocks, making some commentators and investors wonder whether this time is different , or rather something ugly is brewing under the surface.

Free money? No thanks.

Last but not least… Europe. Despite all the efforts by the ECB to boost lending and kickstart demand in the Eurozone via yet again another (T)LTRO, European banks have actually shown little interest in borrowing further funds at zero, with a very low take up on Thursday. Some wonder whether European banks would rather wait for the Asset Quality Review to be out of the way.

Looking at the one way traffic in European inflation break-evens, the cause is more likely to lie in the lack of credit from European corporates, who see very little demand for their goods, and would rather stand by than increase their debt burden. As the case of Japan teaches us, there is only so much that printing money can do, when risk aversion is still high and no structural reforms have been made. Yes, the recent slide in the EUR will provide some breathing space, but ultimately the ball will be in the politicians’ court. Which is not a happy thought.

Euro Inflation BE and China data – FT Alphaville

As Dr. El-Erian mentioned in his latest post, the list of risks and uncertainties is rather long and the “buoyant optimism pervading financial markets may prove to be justified. Unfortunately, it is more likely that investors’ outlook is excessively rosy.”.

I would tend to agree.

Pingback: O Inflation, Inflation! Where art thou Inflation? | MacroCentral.com